GRAND OR petty corruption, fake or faked SAROs — which have been hogging headlines of late — are not the end of the story.

These faked SAROs or Special Allotment Release Orders, along with other accountable forms covering the release of millions of pesos in public funds, are just a sliver of many other systemic flaws and weaknesses in the systems and processes of the Department of Budget and Management (DBM).

In fact, in the Commission on Audit (COA)’s view, these “systems errors” are “not indicative of sound internal control practice” at DBM, the veritable custodian of the national purse.

By all indications, these flaws in DBM’s system for managing SAROs, as well as Notices of Cash Allocation (NCAs), among others, have precisely allowed malefactors, possibly inside and outside the agency, opportunities to manufacture fake or faked documents that apparently lead to funds not reaching the intended beneficiaries.

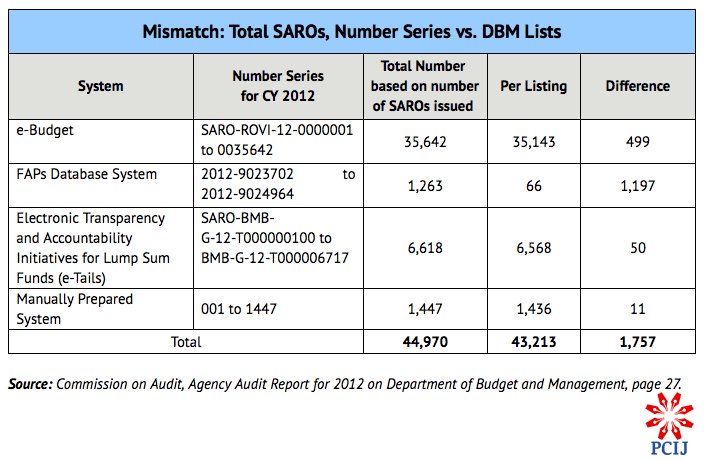

Mismatch: Total SAROs, Number Series vs. DBM Lists

SAROs, by DBM circulars, are documents covering “a specific authority issued to identified agencies to incur obligations not exceeding a given amount during a specified period for the purpose indicated. It shall cover expenditures the release of which is subject to compliance with specific laws or regulations, or is subject to separate approval or clearance by competent authority.”

NCAs, meanwhile, are documents covering “cash authority issued quarterly by the DBM to central, regional and provincial offices and operating units to cover the cash requirements of the agencies.”

Red flags since 2010

COA’s latest agency report on DBM notes that there are “spoiled” or “cancelled” SAROs, SAROs with “skipping numbers”, SAROs counted “per box” and not “per piece”, and even “shredded” SAROs gone to the great beyond.

COA’s agency audit of DBM for 2012 reiterated only the same bigger, messier context of “systems errors” in the Budget Department’s management of SAROs and NCAs that have been exposed again and again since 2010.

Topping the list of 19 various adverse observations that COA raised in its 2012 audit of DBM is a damning statement of doubt about the “completeness and accuracy” of the Budget Department’s system for releasing SAROs and NCAs.

Tally of Cancelled SAROs

COA’s second adverse comment: “Deficiencies in the preparation and submission of Report of Accountability for Accountable Forms (RAAFs) for SAROs and NCA forms and security papers.”

COA raised a red flag in no uncertain terms: The delayed or non-submission to state auditors by DBM officials of these accountability reports could only mean “the possibility of (their) fraudulent use is not eliminated.”

As far back as two years ago, COA had cited this and other problems with “systems errors” in DBM in its agency audit for 2011 and 2010.

In its 2011 audit report on DBM, COA had noted that up to 3,158 SAROs were unaccounted for, bore the same number, or had skipped numbers.

In its 2010 audit report, COA said DBM “failed to account for 6,873 SAROs, hence the actual/total allotment released could not be accounted for/verified.”

Spoiled, cancelled

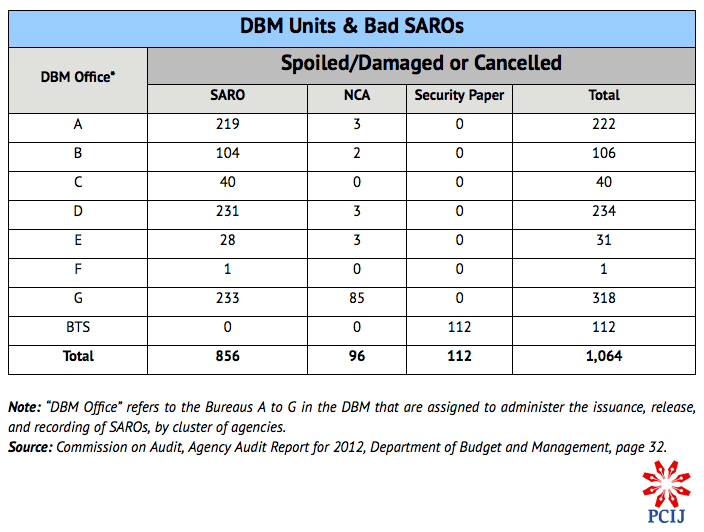

Aside from fake or faked SAROs, there are also “skipping” SAROs, on account of “gaps” in the numbering sequence of SAROs. There are “spoiled/damaged” or “cancelled” SAROs as well. Many had not been defaced or marked as bad SAROs, while some others could not be produced anymore.

In 2012, most of at least 1,064 SAROs reported to be “spoilage” or “cancelled” were not marked as “cancelled” or perforated, according to procedures prescribed in DBM’s own Department Order No. 2011-12 pertaining to “Accountability for SAROs and NCA Forms and Security Paper.”

Issued on Oct. 4, 2011 by Budget Secretary Florencio ‘Butch’ Abad, it spelled out rules on “the issuance, receipt, safekeeping, and reporting” of SAROs, NCAs, and other accountable forms in DBM.

Yet when state auditors asked for copies, DBM officials said that they had destroyed some of these spoiled or cancelled SAROs.

They could not, however, produce proof they actually did so. Instead, they told COA that “due to the confidentiality of release documents, some of the spoiled SAROs were shredded, hence no longer available for inspection.”

Balances not clear

The apparently messy system DBM has for tracking the number series and values of SAROs has resulted in errors in the computation of the ending and beginning balances of funds across quarterly periods, in the case of some DBM directors in charge of SARO releases.

For instance, two DBM administrative officers accounted for SARO issuances “using per box as a unit of measure instead of per piece,” which, COA noted, resulted in the “non-determination of the correct and accurate balance of SAROs” in their control.

Other DBM directors used “per piece” as reference for unit count for SAROs and NCAs, however.

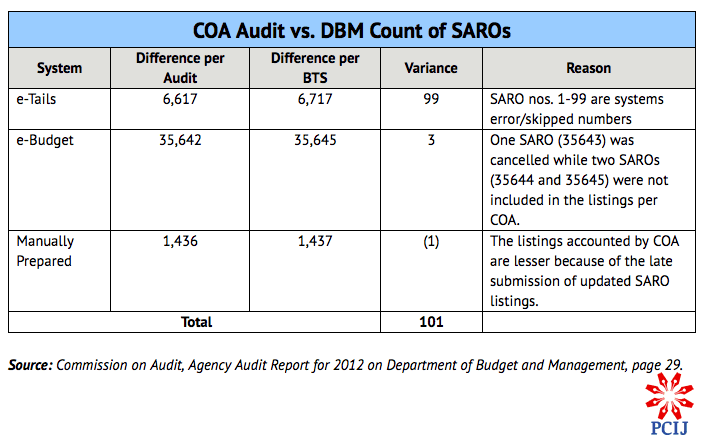

COA Audit vs. DBM Count of SAROs

Meanwhile, most of the DBM administrative officers submitted their accountability forms for the SAROs and NCAs under their watch well beyond deadline.

They finally gave COA copies of their accountable forms late by four to 115 days past deadline.

More findings

The 2012 COA report on DBM listed other “systems errors” in the DBM’s handling of “accountable forms” such as SAROs and NCAs:

- “The reporting and monitoring system in the release of SAROs and NCAs does not include controls on the number sequence, hence, gaps were noted in the number series of SAROs and NCAs issued, casting doubt on the completeness of the listing.”

- “There was no monitoring being made on SAROs and NCAs by the number/number series issued by the amount of releases, except for the manually prepared SAROs and NCAs.” The absence of such monitoring system has resulted in “gaps in the number series of SAROs and NCAs issued.”

- “The (a) delayed/non-submission to COA of the RAAFs for SAROs, NCAs, and security papers: (b) differences in the quarterly beginning balances; and (c) the use of per box as unit of measure in accounting for SAROs, have resulted in the non-determination of the correct balance of Accountable Forms (AFs) in the possession of the Accountable Officers.”

- In the DBM Central Office, “spoiled/damaged accountable forms were not marked ‘cancelled’ or perforated as required” under DBM Department Order No. 2011-12.”

Four systems

DBM’s messy system for managing SAROs and NCAs is largely the result of its use of four application systems in the preparation of the budget of the national government, and in releasing and monitoring of allotments and cash programs.

These four systems are:

- Electronic Budget System (e-Budget);

- Foreign-Assisted Projects (FAPs) Database System;

- Electronic Transparency and Accountability Initiatives for Lump-Sum Funds (e-TAILS) Database System; and

- Manually Prepared System (MIS).

Each system, COA said, “has its own number series.” Thus, to account for all the SAROs and NCAs issued for the year, COA said “a listing of all issuances of SAROs and NCAs per system should be made.”

For the year 2012, COA reported that DBM’s Budget Technical Service (BTS) disclosed that there were 44,970 SAROs with total amount of P1,076,236,898,308.34 (or P1.07 trillion) and 51,758 NCAs worth a total of P1,370,194,118,945.20 (or P1.37 trillion) that had been released under the four applications.

But COA said that a comparison of the SAROs based on the series and number of SAROs per listings” showed a difference of 1,757 SAROs that could not be accounted for.

Skipping numbers

The missing or unaccounted for SAROs include 499 issued under the e-Budget system; 1,197 under the FAPs Database System; 50 under the e-TAILS system; and 11 under the Manually Prepared System. In all, 1,757 SAROs unaccounted for.

COA likewise noted “gaps in the number series of NCAs for the e-Budget and e-TAILs systems” using only “a sample of NCA issuances for January 2012.”

DBM Units & Bad SAROs

According to the COA report, an unnamed DBM-BTS official said that “there was no monitoring made on SARO and NCA by the number/number series issued but by the amount of releases, except for the manually prepared SAROs and NCAs.”

Moreover, COA quoted the official as saying that “the gaps in the number series of SAROs and NCAs which were noted in audit were considered systems errors, which cannot be accounted since the system is being used nationwide.” The official explained that “only the manually prepared SAROs and NCAs were monitored because the number series were controlled and recorded in the logbook of BTS.”

But a different, and truly messy, picture emerges for the other application systems of DBM. For one, the persons in charge of the other systems were simply not in the habit or practice of informing each other about the assigned numbers and amounts involved in the SAROs and NCAs they respectively administer.

COA observed, “(The) personnel of Incuventure Partners Corporation who administer the systems confirmed that the gaps noted in the SAROs and NCAs were indeed caused by errors in the systems.”

Sadly for taxpayers, however, “these gaps were not reported to the concerned office because they were not required by (DBM) Management,” COA quoted the Incuventure official as saying.

COA recalled that in its agency audit of DBM for 2011, “these differences in the SAROs that had been raised… and the reasons cited were skipping of the SAROs and numbering in the system and “DUMMY” or Adjustment SAROs, which were done only in the system.”

Reports not shared

“Among the audit recommendations was for the DBM to revisit the process of assigning SARO number and install measures that SARO releases were all accounted for,” COA said. “To date, however, the same conditions were noted by the audit team.”

COA continued: “The non-reporting of the Administrator of the systems to BTS of the gaps in the number series of SAROs and NCAs cast doubt about the completeness and accuracy of SAROs and NCAs issued and is not indicative of sound internal control practice.”

An accounting and reporting of the gaps in SARO and NCA number series “should be in place to fully ensure the completeness and accuracy of SARO and NCA issuances,” it added.

In reply to COA’s queries, on March 21, 2013, the DBM Undersecretary for Operations (Mario L. Relampagos) “assured that appropriate control system/measures are in place for fund releases through SAROs and NCAs and explained that the gaps in the number series… were due to cancellation and system’s error.”

The Undersecretary told COA that the cancelled SAROs were included in soft copy provided to state auditors, including:

- e-Budget system: 225 “cancelled” SAROs and 277 “inadvertent inclusions”;

- FAPs: 1 cancelled SARO and 1,196 inadvertent inclusions;

- E-TAILs: 30 cancelled SAROs and 119 inadvertent inclusions; and

- Manually Prepared System: 10 cancelled SAROs and zero inadvertent inclusions.

In addition, DBM acknowledged that at least 338 NCAs were cancelled, and another 653 were “inadvertent inclusions” in its application systems in 2012.

Contrary to DBM’s claim, however, COA said that “verification of the data received by our office revealed that the cancelled SAROs were not in the soft copy submitted” by DBM.

Still, the DBM Management clarified that “the existing systems have behavioral limitations resulting in some errors in the numbering sequence.”

Click, click, click?

Such “behavioral limitations” reportedly include errors like double or multiple clicks of the “approved” button in the application systems, a clear vulnerability of the system to parties given to either plain mischief or grand larceny.

“The numbers are missed during the approval process of SAROs and NCAs, thus creating gaps in the number series, which happens when the ‘approved’ button in the systems are clicked more than once,” DBM told COA.

On Jan. 24, 2011, DBM had decided to outsource the software maintenance of its four application systems for fiscal year 2011-2012 to a relatively new IT solutions company called Incuventure Partners Corporation. The total contract cost: P16,694,441.07.

In the project documents, DBM said it announced the public bidding of the contract in October 2010 but that Incuventure submitted “the only responsive bid” at the time the bids were opened in November 2010.

Yet for all the “systems errors” that marked its services for DBM, Incuventure, in joint venture with Computer Network Systems Corporation, won a second contract worth P39.5 million from DBM in August 2013. — PCIJ, December 2013